Unlock precision risk insights for trading desks and quant strategies

The Axioma Equity Factor Risk Models: Trading Horizon delivers precise portfolio risk exposures and forecasts for ultra-short investment horizons when the markets move abruptly and sharply change direction.

Available in two variants:

US Trading Horizon (US5.1-TH)

Download factsheet

Worldwide Trading Horizon (WW5.1-TH)

DOWNLOAD FACTSHEETWhy Trading Horizon Models?

Get daily insights

Capture the day-to-day changes in risk of the trading book and other portfolios with short investment horizons

Manage high-frequency strategies

Accurately capture risk/return trade-offs for fast moving alpha signals and high turnover strategies

Rebalance with confidence

Understand the trade-off between risk and market impact/slippage and improve portfolio implementation and execution

Understand risk drivers

Get insights into the event-driven risk stemming from earnings announcements, short-squeezes and other infrequent events

Who is the Trading Model for?

Hedge fund managers

Quantitative asset managers

Algo traders

Sell-side managers

Risk managers

Structuring desks

New factors in Version 5.1 vs previous version (4.0)

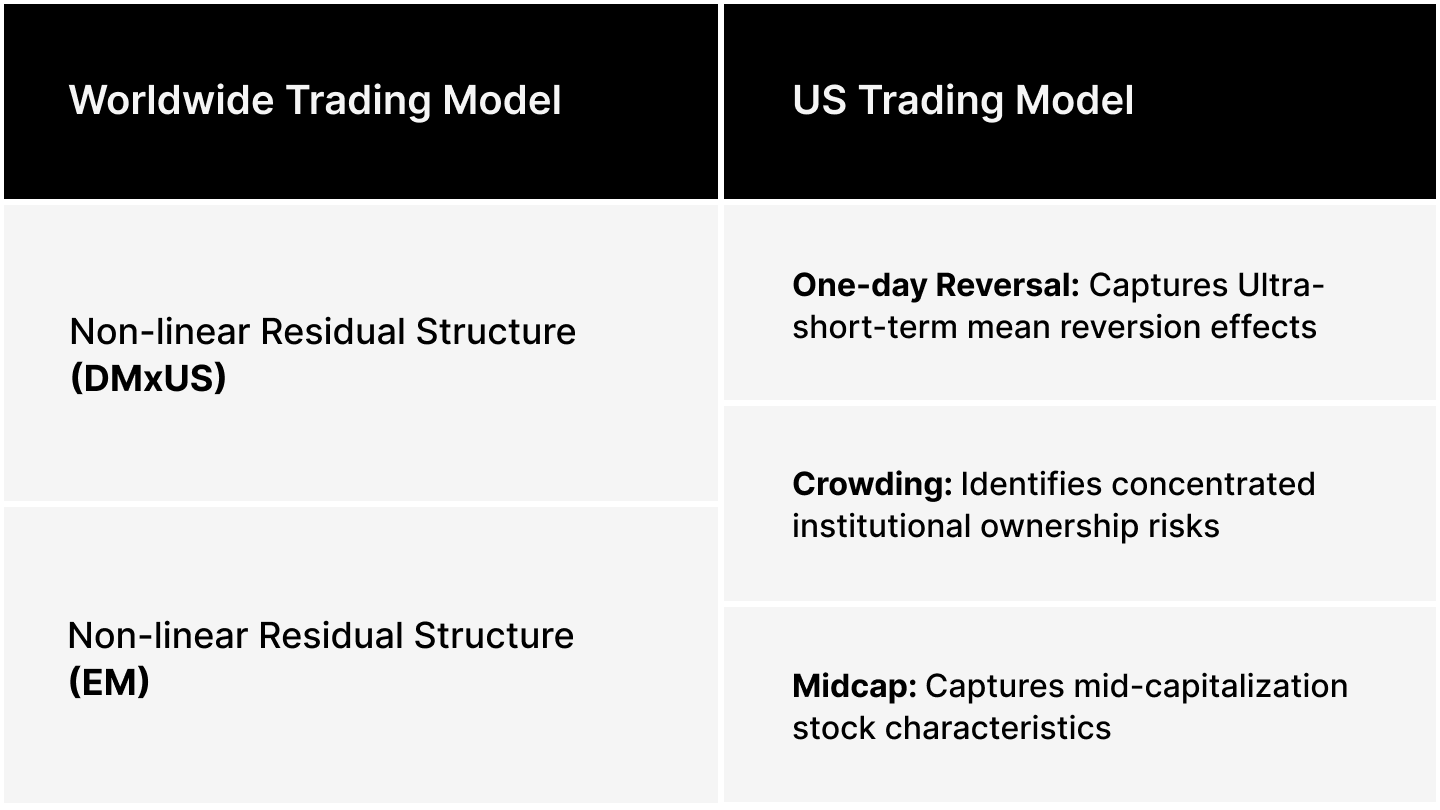

- Short Interest: Risk and return impact based on how heavily a stock is shorted

- Opinion Divergence: Measures lack of consensus among investors based on unusual trading volume

- Downside Risk: Captures negative or uncompensated risk including downside volatility and recent maximum returns

- Investment: Measures asset growth, sales growth, and inventory growth

- Non-linear Residual Structure: Finds higher-order explanatory factors in residual returns to capture hidden risk exposures

Worldwide vs US Trading Model (v5.1)

The Trading Model offers faster reaction to and faster retreat from market disruptions

Related products

Axioma Equity Factor Risk Models

Flexible and intuitive equity risk models backed by proprietary research

Axioma Portfolio Optimizer

Advanced portfolio construction software for research and analysis

Axioma Risk

Cloud-native, SaaS risk management solution for a single, consistent view of risk

Contact us

Related Content